How to Receive USD Payments in Asia as a Business

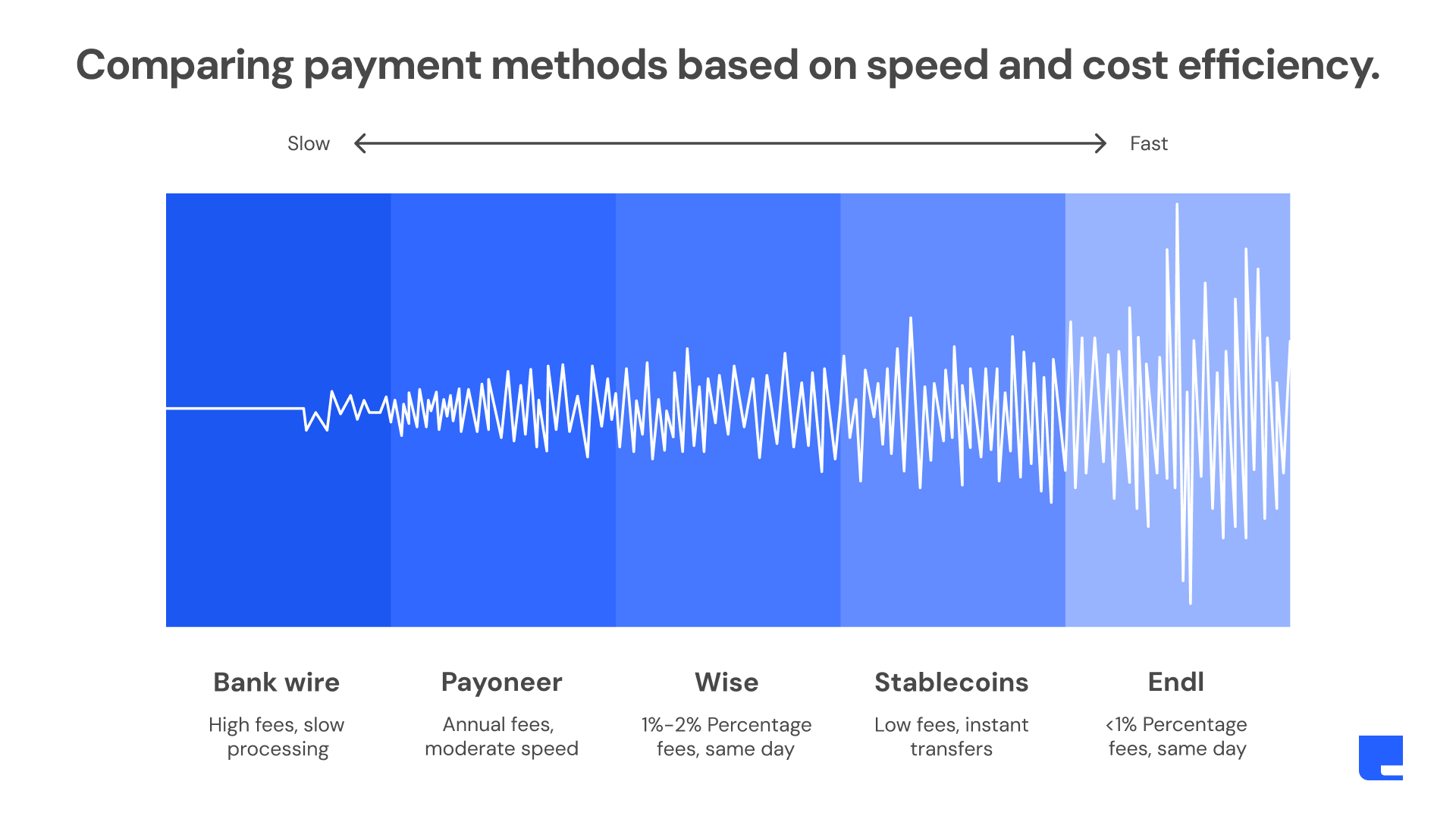

Asian companies frequently work with US clients and partners, but receiving USD payments through traditional bank wires is often slow and expensive. Standard SWIFT transfers typically take 3–5 days and cost 3–5% once FX markups and intermediary fees are included.

Modern alternatives—such as virtual USD accounts, fintech platforms, and stablecoins—allow businesses to receive USD faster, hold it without forced conversion, and use it immediately for operations or supplier payments.

Why Receiving USD in Asia Is Difficult with Traditional Banks

Without the right tools, Asian businesses face several challenges when receiving USD:

- Banks charge high FX spreads on incoming USD

- Buyers hesitate to send money to foreign bank accounts

- Payments are delayed or held by intermediaries

- Limited transparency until funds fully settle

Virtual USD accounts address these issues by providing US bank account and routing numbers, making payments appear local to American customers.

Easy Ways to Receive USD in Asia

1. USD Virtual Accounts

USD virtual accounts provide US account and routing numbers that customers can pay into via ACH, wire, or PayPal, just like paying a US-based business.

- Same-day or near-instant settlement

- 0% FX loss on receipt

- Ideal for dropshippers, freelancers, and e-commerce sellers

2. Fintech Platforms

- Payoneer – Free USD receiving accounts, widely used with Shopify and Amazon

- Wise – Fast USD receipts with low FX conversion costs

- Airwallex – Multi-currency accounts designed for larger or scaling businesses

These platforms reduce delays compared to traditional banks and simplify cross-border collections.

3. Stablecoins (USDC / USDT)

Stablecoins are cryptocurrencies pegged to the US dollar.

- Settlement in minutes

- Fees typically under 0.5%

- Easy conversion to local currency

They are especially useful for fast payouts or paying international suppliers.

4. Endl-Style Platforms

Platforms like Endl combine USD virtual accounts with multi-currency wallets and stablecoin support.

- Receive USD same day

- Pay suppliers in 200+ countries

- Real-time transaction tracking

- Total fees often under 1%

This approach is well suited for e-commerce businesses managing both US customers and Asian suppliers.

Simple Steps to Start Receiving USD in Asia

- Choose a platform (Endl or Wise for quick setup)

- Register online and upload business documents (1–2 days)

- Obtain USD account details and share them with US clients

- Configure automatic transfers to your primary account

- Confirm KYC and AML compliance

- Start with a small test payment before scaling

Conclusion

Receiving USD payments in Asia no longer needs to be slow or expensive. With virtual accounts, fintech platforms, and stablecoins, businesses can get paid faster, reduce fees, and operate more efficiently with US customers.

FAQs

Q1: Why do traditional bank wires perform poorly for USD receipts in Asia?

SWIFT transfers involve multiple intermediaries, leading to 3–5 day delays and fees of $25–$50 per $1,000, plus FX markups.

Q2: How do virtual USD accounts make payments feel local?

They provide US routing and account numbers, allowing customers to pay via ACH or wire as if sending money to a US business.

Q3: What advantage do stablecoins like USDC have over Payoneer or Wise?

USDC enables near-instant blockchain transfers with fees under 0.5%, which can then be converted quickly to local currency.

Q4: Can Endl handle payments to Asian suppliers after receiving USD?

Yes. Endl allows businesses to receive USD same day and pay suppliers in over 200 countries with real-time tracking and fees under 1%.

Q5: Are these platforms compliant for Asian businesses?

Yes. Platforms like Endl, Wise, and Circle operate under regulatory frameworks in the US, EU, and Asia and require full KYC and AML verification.