Stablecoin to Bank Account Payouts: Complete Guide for Businesses

Stablecoins such as USDT (Tether) and USDC (USD Coin) allow businesses to receive international payments quickly and at low cost. Many global clients now pay companies directly in these digital dollars.

However, businesses still need to convert stablecoins into bank fiat to pay taxes, salaries, rent, and local suppliers. This guide explains the full process—timelines, costs, risks, and best practices—so companies can move from stablecoins to bank accounts efficiently.

Why Businesses Need Stablecoin-to-Bank Payouts

Stablecoins live on blockchains, which makes them ideal for fast cross-border transfers but not always practical for day-to-day operations. Banks are still required for payroll, accounting, and regulatory reporting.

Stablecoin-to-bank payouts combine:

- Blockchain speed (minutes to receive funds)

- Bank usability (fiat in a local account)

End-to-end, the process typically takes 1–48 hours, far faster than traditional SWIFT wires that take 3–5 days.

Key Benefits for Companies

- Lower total costs: Typically 0.5–1.5%, compared to 3–7% with banks

- Price transparency: Clear FX rates and fees shown upfront

- No foreign bank account required: Operate from Asia, Europe, or anywhere globally

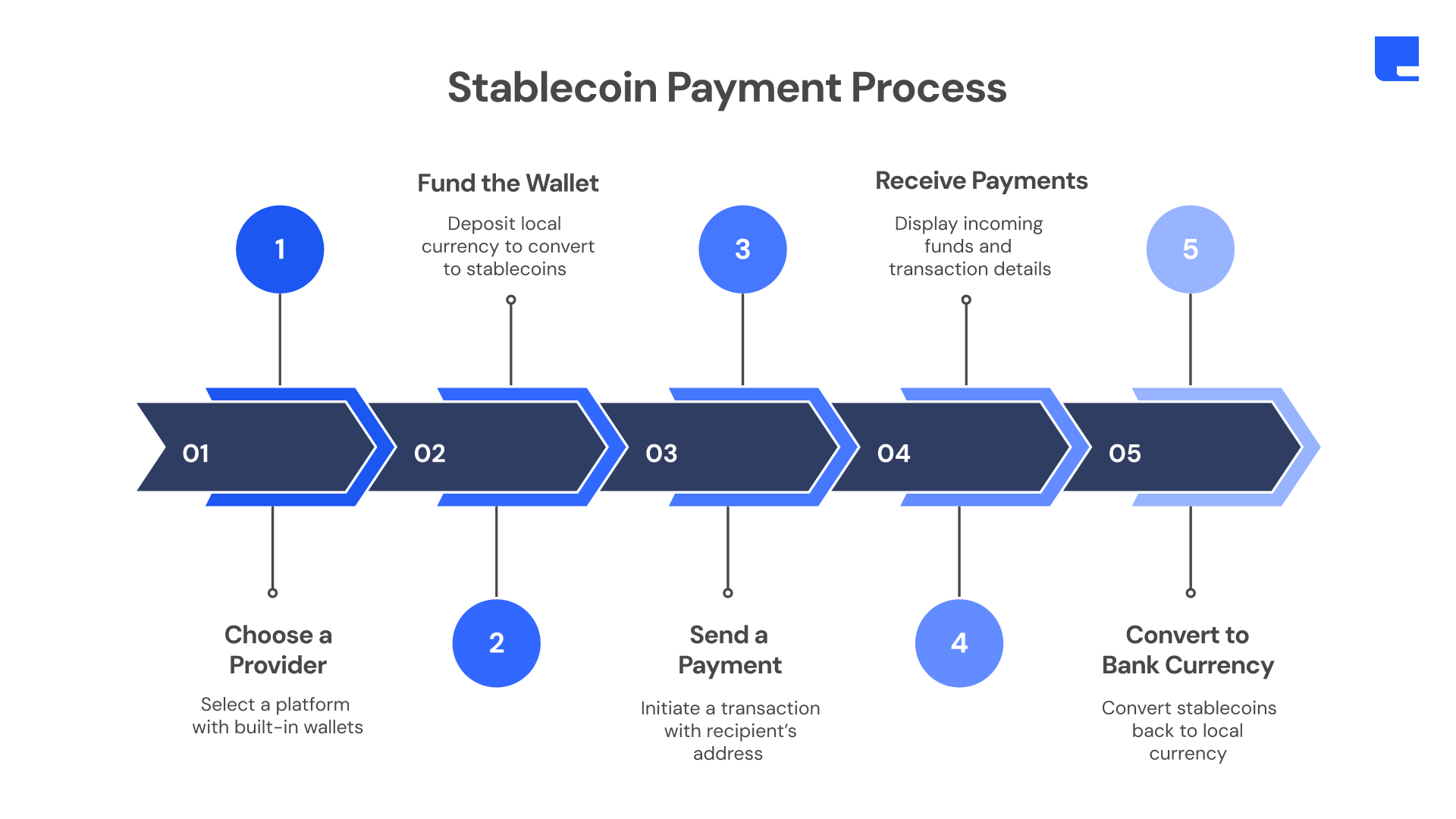

Detailed Step-by-Step Process

Step 1: Prepare Your Setup (One-Time)

Choose a trusted platform that supports:

- USDT and USDC

- Local bank withdrawals

- Business accounts with compliance controls

You’ll need standard KYC/AML documents:

- Business registration

- Proof of address

- Owner or director ID

- Expected transaction volumes

Initial verification usually takes 1–3 days. Link your bank account using local formats such as IBAN (EU), routing/account number (US), or IFSC (India). Always test with a small amount first.

Step 2: Receive and Secure Stablecoins

Clients send stablecoins (e.g., $5,000 USDC) to your wallet.

- Verify receipt using a blockchain explorer (e.g., Tronscan or Etherscan)

- If funds arrive in an external wallet, transfer them to your conversion platform

Common networks:

- Tron – ~$1 fees, popular for regular business payments

- Solana – Extremely fast processing

- Polygon – Low fees, ~2-minute settlement

- Ethereum – High security, higher fees during peak times

Step 3: Convert Stablecoins to Fiat

In the platform dashboard:

- Go to Convert or Trade

- Select Sell USDT/USDC → Target currency (USD, EUR, INR, PHP, etc.)

- Review the rate (often market rate minus 0.1–0.5% spread)

- Execute the conversion

Fiat balances usually appear instantly.

Real-world example:

An Indonesian software team receives 15,000 USDT monthly from US and EU clients.

- Stablecoins arrive via Tron (fee under $1)

- Converted to IDR at a 0.3% spread

- Total cost (conversion + withdrawal): ~$75

With SWIFT wires, the same flow took 5 days and cost ~$450 in fees and FX losses. Funds now reach their Mandiri Bank account the next morning, enabling timely salary payments for 20 developers.

Step 4: Withdraw to Your Bank Account

From your fiat balance, choose Withdraw → Bank transfer.

Examples by region:

- US: ACH same-day (often free) or wire in 1 day ($15–25)

- Asia (India, Philippines, Vietnam): IMPS/NEFT or local rails, instant to 1 day

- Europe: SEPA Instant in seconds to 1 hour (low fixed fees)

Platforms often batch withdrawals for efficiency.

Step 5: Verify and Record

- Track status: processing → sent → cleared

- Confirm receipt in your bank (1–24 hours)

- Save records: transaction hash, exchange rate, fees

- Record conversions as USD-denominated sales for accounting and tax reporting

Full Timing and Cost Example ($10,000 USDT)

- Receive: Instant, $0.50 network fee

- Convert: Instant, $30 (0.3%)

- Withdraw (SEPA): ~1 hour, $0.50

Total: ~2 hours and $31 (0.31%)

Bank wire alternative: ~3 days and $300+ (3%)

Common Challenges and Solutions

- Irreversible transactions: Always double-check wallet addresses

- Weekend delays: Use instant payment rails where available

- Scaling risk: Start with $1,000 limits and increase gradually

- Tax treatment: Log conversions carefully as taxable events

- Peg monitoring: Rare deviations can occur—monitor large balances

- Compliance flags: Keep business documents updated

Advanced Tips for Businesses

- Automate rules (e.g., auto-convert balances over $5,000)

- Batch conversions weekly to reduce fees

- Keep a mix of fiat and stablecoins for flexibility

- Integrate with QuickBooks or Xero for automated bookkeeping

- Use role-based access for teams

- Enable insurance or custody protections where available

Conclusion

Stablecoin-to-bank payouts turn digital dollars into usable bank funds reliably and quickly. Businesses handling international payments can save significant time and cost by combining stablecoin speed with local banking rails. Start with a $100 test transfer, confirm the flow, and scale with confidence.

FAQs

Q1: How long does it take to convert USDT or USDC to bank fiat?

Typically 1–48 hours end-to-end: instant receipt, instant conversion (0.1–0.5% spread), and bank withdrawal via ACH, SEPA, or IMPS in seconds to one day.

Q2: What documents are required for business KYC?

Business registration, proof of address, owner ID, and transaction volume estimates. Initial approval usually takes 1–3 days.

Q3: Which blockchain networks are best before conversion?

Tron (~$1 fees), Solana (fastest), Polygon (low-cost), or Ethereum (secure but higher peak fees).

Q4: What is the total cost for a $10,000 stablecoin-to-bank payout?

About $31 (0.31%), compared with $300+ (3%) via traditional bank wires.

Q5: Are stablecoin conversions taxable?

Yes. Treat conversions as USD-denominated sales and keep transaction hashes, rates, and fee records for accounting and taxes.