Stablecoin vs SWIFT for International Transfers – Which Is Cheaper?

The conventional messaging system used by banks for international payments is called SWIFT. Although it links more than 11,000 institutions, it depends on several intermediary banks, which causes costs and delays. On blockchain networks, stablecoins like USDT and USDC move immediately and are frequently settled in a matter of minutes. Companies evaluate them according to their overall cost, which takes into account fees, exchange rates, and the time worth of money.

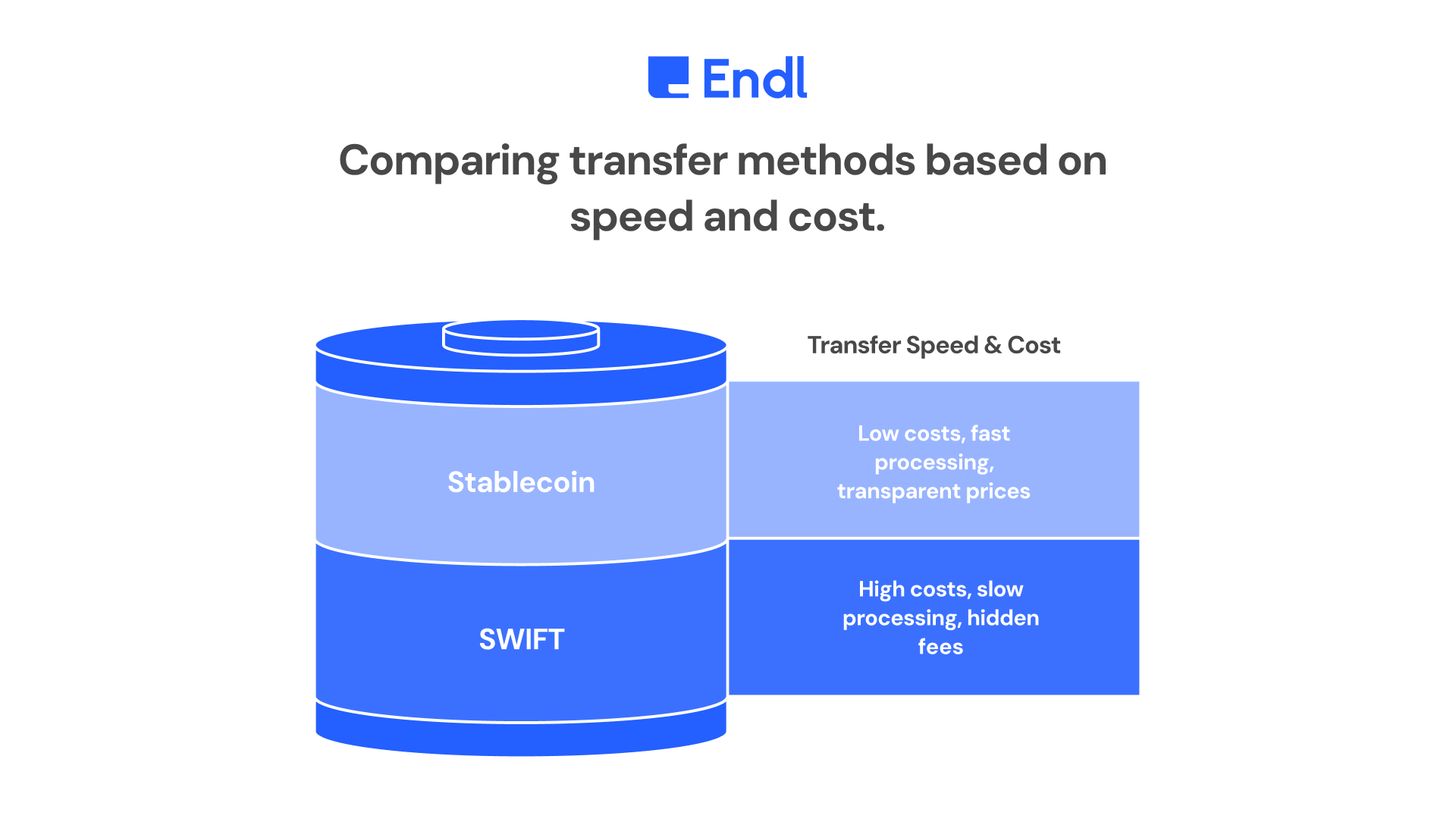

Breaking Down SWIFT Costs

A typical SWIFT transfer involves:

- Sending bank fee: $25–50

- Intermediary banks: $10–25 each (often 1–3 banks)

- Receiving bank fee: $10–20

- Currency exchange markup: 2–4% above market rates

For a $10,000 transfer, total costs often hit $250–500 (2.5–5%). Hidden extras include amendment fees ($25–40), investigation costs for delays ($25–50), and opportunity costs from funds tied up for 1–5 business days. Weekends and holidays add more waiting.

Breaking Down Stablecoin Costs

Stablecoin transfers have two main parts: on-chain movement and fiat conversion.

- Network fees: $0.01–5 (Tron cheapest, Ethereum is higher during peaks)

- On/off ramps: 0.1–0.5% for buying and selling stablecoins

- Bank withdrawal: $0–25

Same $10,000 example: $1 network fee + $30 ramps + $10 bank = $41 total (0.41%). No intermediaries, 24/7 availability, and settlement in seconds to minutes.

Real-Life Example

A European SaaS company pays Brazilian developers $20,000 monthly.

SWIFT route: €40 sender fee + two intermediaries ($30) + 3% FX markup (€600) + three-day delay = €700 total cost. Developers wait over the weekend.

Switching to USDC on Polygon: $2 network fee + 0.3% ramps ($60) = $62 total. Payment is confirmed in two minutes. Developers cash out locally the same day. Company saves €638 per month (€7,656 annually), enabling faster iterations and happier teams.

Endl and Similar Platforms Make Comparisons Easier

Because it manages the entire stablecoin flow for companies, including bank linkages, conversions, and wallets. Stablecoins are as simple as SWIFT but more affordable and quicker for frequent transfers since they offer transparent upfront prices, real-time tracking, and compliance.

When Stablecoins Win on Cost

- High volume: Fixed low fees scale better than SWIFT’s percentage-based pricing

- Frequent or small payments: $100 transfers cost pennies versus SWIFT minimums

- Multi-country payouts: No per-corridor banking relationships required

- Volatile regions: Ability to hold USD value without local FX risk

Annual savings for $100K monthly transfers: SWIFT $30K+, stablecoins ~$5K.

When SWIFT Might Still Make Sense

- Very large one-off transfers above $1M where banks may waive fees

- Highly regulated industries dependent on legacy rails

- Recipients without access to crypto ramps in certain regions

Other Considerations Beyond Price

Unlike SWIFT’s limited transparency, stablecoins provide real-time visibility through blockchain explorers. They can be programmed for batching or escrow. SWIFT GPI improves tracking but does not achieve cost or speed parity.

Example from real life: Ten Chinese vendors receive $5,000 monthly from an Indian global seller ($50K total).

SWIFT: ~$2,000 per month

USDT on Tron: ~$150 per month

Savings finance additional inventory, increasing income by over 20%. Instant confirmation is preferred by suppliers over bank uncertainty.

Conclusion

For most businesses, stablecoins are more affordable than SWIFT. They are a clear winner for recurring cross-border payments in supply chains, e-commerce, and freelancing due to faster settlement and 80–90% lower costs. SWIFT remains suitable for large, infrequent institutional transfers. As on- and off-ramps mature, the cost gap continues to widen. Many companies begin by testing small transfers to validate savings directly.

FAQs

Q1: How much cheaper are stablecoins vs SWIFT for a $10K international transfer?

Stablecoins cost about $41 total (0.41%) compared to $250–500 (2.5–5%) via SWIFT, delivering 80–90% savings with settlement in minutes instead of days.

Q2: What hidden costs make SWIFT more expensive than it appears?

Intermediary bank fees, FX markups, amendment charges, investigation fees, and opportunity costs from delayed settlement.

Q3: Which networks keep stablecoin fees lowest for business transfers?

Tron, Polygon, and Solana offer the lowest fees, while Ethereum costs rise during peak usage.

Q4: When does SWIFT still outperform stablecoins on cost?

Very large one-off transfers, legacy-only regulated environments, or regions without reliable crypto ramps.

Q5: How do platforms like Endl simplify stablecoin adoption?

They manage wallets, conversions, bank links, pricing transparency, and real-time tracking, making stablecoin payments operationally similar to SWIFT but faster and cheaper.