Why Businesses Are Switching to Stablecoin Payments

Stablecoins such as USDT (Tether) and USDC (USD Coin) are digital currencies pegged to the US dollar, typically maintaining a value close to $1. Unlike volatile cryptocurrencies, stablecoins are designed for payments, not speculation.

Businesses across industries are increasingly using stablecoins because they solve long-standing problems with international transfers—high fees, slow settlement, and limited access—at a time when global trade, freelancing, and remote work are expanding rapidly.

High Costs of Traditional Bank Payments

Traditional bank wires and systems like SWIFT come with multiple layers of fees:

- Sender fees of $25–50

- Intermediary bank charges

- Receiving bank fees

- 2–4% FX markups above market rates

For a business sending $10,000 to international vendors each month, this can result in $300–500 lost per payment.

Stablecoins reduce these costs dramatically. By using blockchain networks, transaction fees are typically under $1–5, even for international transfers.

Slow Processing and Cash Flow Issues

Bank transfers often take 1–5 business days due to time zone differences, compliance checks, and bank reconciliation processes. These delays can disrupt cash flow, delay supplier payments, and complicate financial planning.

Stablecoins settle in minutes on networks like Solana or Tron, with near-instant confirmation. Faster settlement improves liquidity and strengthens relationships with suppliers and freelancers who depend on timely payments.

Limited Access and Currency Risks

In countries with capital controls, currency volatility, or restricted access to USD banking, receiving and holding dollars can be difficult.

Stablecoins provide a digital alternative to USD that businesses can:

- Invoice in

- Hold without immediate FX losses

- Convert to local currency when rates are favorable

Real-world example (Turkey):

A Turkish marketing agency serving US and EU clients faced delayed USD receipts and high costs due to local currency volatility. Bank wires took 3 days and cost about 4% per transfer.

After switching to USDC, client payments now arrive in 10 minutes. The agency pays freelancers globally, holds USDC for stability, and converts only what’s needed for local expenses. Monthly savings exceed $400, while cash flow predictability improves despite economic uncertainty.

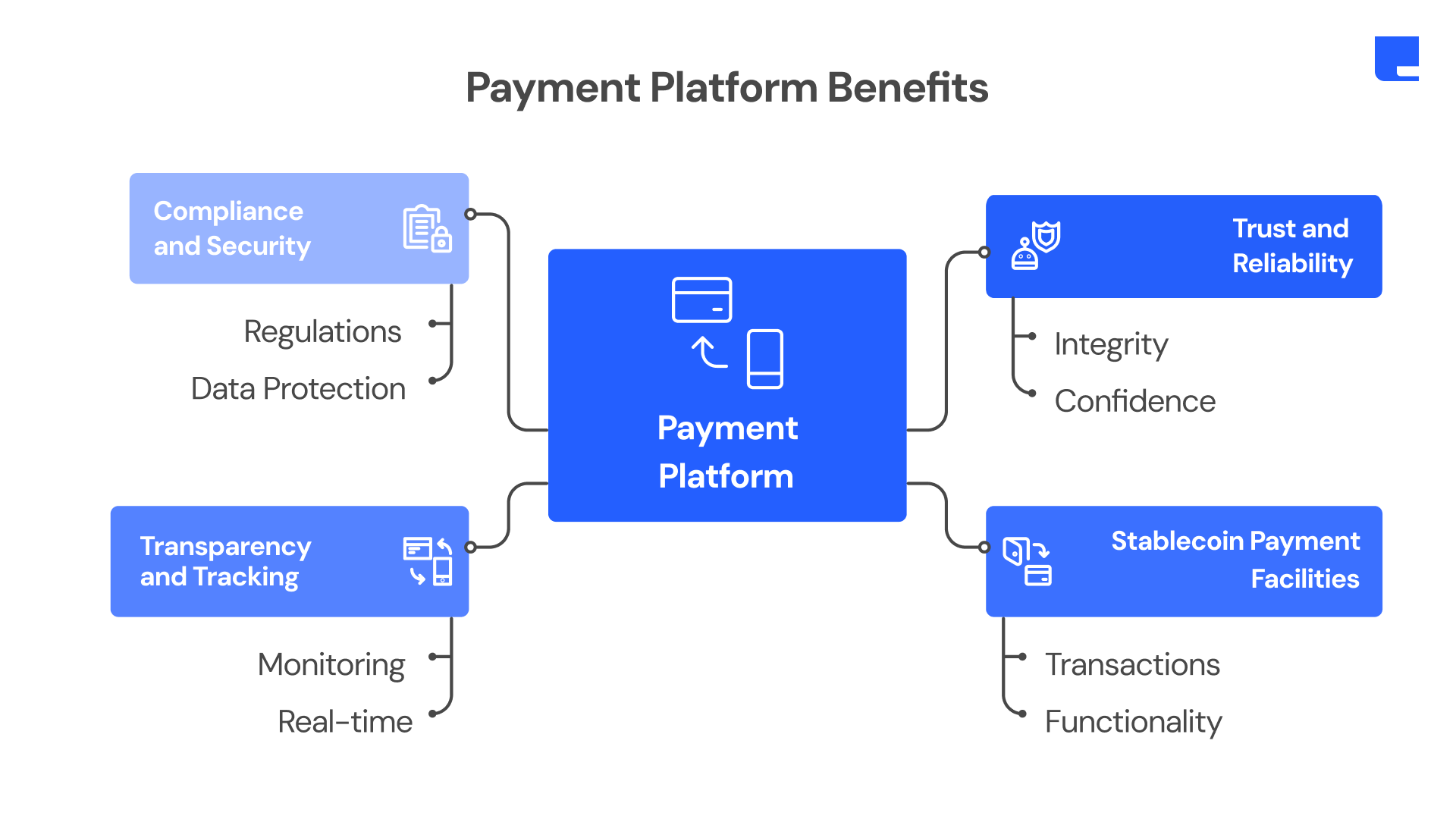

Platforms Like Endl Support the Switch

Business-focused platforms like Endl make stablecoin adoption easier by offering:

- Multi-currency wallets holding USDT/USDC alongside fiat

- Built-in compliance features

- Real-time transaction tracking

- Simple on/off ramps to convert stablecoins to bank funds

For dropshippers, agencies, and exporters handling regular international payments, this removes technical barriers and simplifies operations.

Greater Transparency and Tracking

Stablecoin transactions are recorded on public blockchains, providing:

- Real-time visibility into payment status

- Immutable transaction records

- Easier reconciliation and auditing

Unlike bank wires, where businesses wait days for confirmation, stablecoin payments are verifiable within minutes.

Compliance and Security Improvements

Modern stablecoin platforms include KYC and AML checks similar to traditional banks. Issuers like Circle (USDC) maintain reserves that are regularly audited, adding confidence for regulated businesses.

Blockchain cryptography makes transactions tamper-resistant, improving overall security when combined with standard safeguards like 2FA and access controls.

Scalability for Growing Operations

Stablecoins scale well for businesses handling high payment volumes, including SaaS companies, remote teams, and e-commerce sellers.

Real-world example (India):

An Indian dropshipping business imports goods from China and sells to the US and UK.

- Before: Bank-based supplier payments cost $50 per transfer, totaling $600 per month, with delays.

- After: Using stablecoins, each supplier payment costs under $5, reducing monthly costs to $60.

Faster supplier payments led to quicker restocking and a 15% increase in revenue, without adding staff.

Challenges and How Businesses Adapt

Stablecoins are not without challenges, but businesses adapt by:

- Starting with small test transactions

- Choosing low-cost, reliable networks

- Monitoring network congestion

- Using compliant platforms for conversions

- Keeping accurate records for taxes and accounting

As regulations evolve, clarity around stablecoin use continues to improve in many regions.

Conclusion

Businesses are switching to stablecoins because the economics make sense. Compared to traditional bank payments, stablecoins are faster, cheaper, and more accessible for regular cross-border transactions. For companies operating globally, they remove unnecessary financial friction and enable more efficient growth.

FAQs

Q1: Why are businesses switching from bank wires to stablecoins like USDT and USDC?

Stablecoins reduce $300–500 fees on $10,000 transfers to under $5 and settle in minutes instead of 1–5 days, improving cash flow and reducing FX losses.

Q2: How do stablecoins help in countries with currency controls or volatility?

They allow businesses to hold digital USD value, invoice globally, and convert to local currency at optimal times—helping firms like Turkish agencies save $400+ per month.

Q3: What platforms make stablecoin adoption easier for teams?

Platforms like Endl provide multi-currency wallets, compliance checks, real-time tracking, and easy fiat conversion without technical setup.

Q4: Are stablecoins secure and compliant for business use?

Yes. With audited reserves (e.g., USDC), blockchain immutability, and integrated KYC/AML, stablecoins meet many business compliance needs.

Q5: How do stablecoins scale for e-commerce or high-volume operations?

They integrate with payment systems for automated payouts, enabling instant, low-cost supplier payments and faster inventory cycles.